Contents

Overview

The concept of the time value of money, while formalized much later, has roots stretching back to ancient thinkers. Aristotle, in his work Politics (circa 350 BCE), critiqued usury, arguing that money is sterile and cannot reproduce itself, thus questioning the legitimacy of interest. However, the idea that money could grow over time was implicitly understood by merchants and financiers throughout the Middle Ages. Formalization began to emerge during the Renaissance, with scholars like Martín de Azpilcueta in 1545 explicitly articulating the principle that a sum of money is worth more today than in the future, a concept crucial for understanding international trade and lending. Later, Isaac Newton, in his role as Master of the Royal Mint, meticulously recorded interest rates, demonstrating a practical grasp of TVM. The development of compound interest formulas by mathematicians like Jacob Bernoulli in the late 17th century provided the quantitative framework that would solidify TVM as a cornerstone of financial mathematics.

⚙️ How It Works

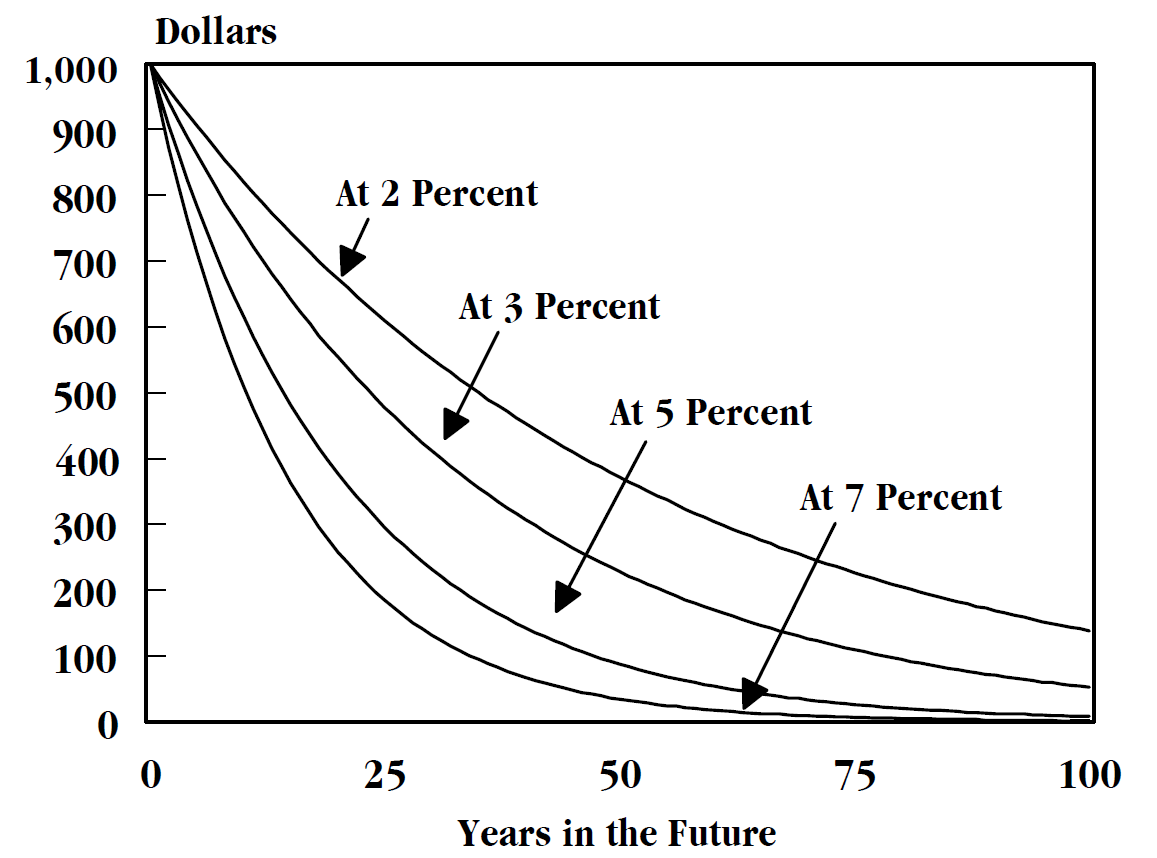

At its heart, the time value of money operates on two primary calculations: future value (FV) and present value (PV). Future value determines what a current sum of money will be worth at a specified future date, assuming a certain rate of return (interest rate). The formula for simple FV is FV = PV * (1 + r)^n, where 'PV' is the present value, 'r' is the interest rate per period, and 'n' is the number of periods. Conversely, present value calculates the current worth of a future sum. The formula for PV is PV = FV / (1 + r)^n. These calculations are fundamental to understanding concepts like annuities, perpetuities, and discounted cash flow (DCF) analysis, which are used to value assets and make investment decisions by bringing future cash flows back to their equivalent value today.

📊 Key Facts & Numbers

The average annual return on the S&P 500 index has historically hovered around 10-12% over long periods, illustrating the power of compounding. A single dollar invested today at a 7% annual return would grow to approximately $19.48 in 45 years. Conversely, a promise of $1,000 in 20 years, with a discount rate of 5%, is only worth about $377 today. The global debt market, a direct application of TVM principles, is valued in the hundreds of trillions of dollars, with the International Institute of Finance reporting over $300 trillion in global debt in 2023. Even a small difference in interest rates, say 1% over 30 years, can mean hundreds of thousands of dollars difference in the repayment of a mortgage. The national debt of the United States, currently exceeding $34 trillion, is a massive testament to the long-term implications of TVM.

👥 Key People & Organizations

While no single individual 'invented' the time value of money, its formalization owes much to economists and mathematicians. Irving Fisher, in his seminal 1930 work The Theory of Interest, provided a rigorous mathematical and economic analysis of interest rates and time preference. John Hicks further refined these concepts in his Value and Capital (1939), integrating TVM into general equilibrium theory. In corporate finance, figures like Eugene Fama and Merton Miller explored the implications of TVM in capital markets, earning them Nobel Prizes. Financial institutions like Goldman Sachs and J.P. Morgan employ legions of analysts who live and breathe TVM calculations daily, while regulatory bodies like the Securities and Exchange Commission (SEC) rely on its principles for asset valuation and investor protection.

🌍 Cultural Impact & Influence

The pervasive influence of TVM is evident in nearly every facet of modern life. It shapes individual financial planning, from saving for retirement using 401(k) plans to understanding the true cost of a car loan. In business, it's the bedrock of capital budgeting, dictating whether a company invests in new machinery or a new product line. The concept is embedded in the valuation of real estate, where future rental income is discounted to determine present worth. Even in less obvious areas, like environmental economics, TVM is used to discount future environmental benefits or costs. The cultural narrative around 'getting rich quick' often ignores TVM, highlighting a societal tension between immediate gratification and long-term financial prudence, a tension often explored in films like The Wolf of Wall Street.

⚡ Current State & Latest Developments

In 2024, the time value of money remains as critical as ever, though its application is increasingly sophisticated. The rise of FinTech companies has democratized access to complex TVM calculations through user-friendly apps and platforms. Machine learning algorithms are now being used to refine discount rates and predict future cash flows with greater accuracy. Central banks globally, including the Federal Reserve and the European Central Bank, continuously adjust interest rates, directly impacting the TVM calculations for everything from mortgages to corporate bonds. The ongoing debate about inflation and its effect on real interest rates keeps TVM at the forefront of economic policy discussions, particularly concerning the purchasing power of future earnings.

🤔 Controversies & Debates

While TVM is a widely accepted principle, its application isn't without debate. A key controversy lies in determining the appropriate discount rate. Critics argue that subjective factors, market sentiment, and varying risk perceptions can lead to vastly different PV calculations, making valuations inherently imprecise. The assumption of constant interest rates over long periods is also frequently challenged, especially in volatile economic environments. Furthermore, some behavioral economists, like Daniel Kahneman, highlight how psychological biases, such as hyperbolic discounting (valuing immediate rewards far more than future ones), often lead individuals to deviate from rational TVM calculations. The ethical implications of discounting future generations' well-being in long-term projects, like climate change mitigation, also spark significant debate.

🔮 Future Outlook & Predictions

The future of TVM will likely be shaped by advancements in artificial intelligence and big data. AI could offer more dynamic and personalized discount rates based on real-time market conditions and individual risk profiles. The increasing complexity of financial instruments, such as cryptocurrencies and decentralized finance (DeFi) products, will necessitate new models for calculating time value, potentially incorporating volatility and network effects. As global economic integration deepens, understanding cross-border TVM implications will become even more crucial. Experts predict a continued emphasis on scenario analysis and stress testing TVM models to account for increasing systemic risks, ensuring financial resilience in an unpredictable world.

💡 Practical Applications

The practical applications of TVM are ubiquitous. For individuals, it's essential for calculating loan payments (mortgages, car loans), understanding the payout of annuities, and determining the future value of savings and investments. Businesses use TVM extensively in capital budgeting to evaluate capital expenditures through methods like Net Present Value (NPV) and Internal Rate of Return (IRR). Financial analysts use it to value stocks and bonds, and for mergers and acquisitions (M&A) to assess the fair price of target companies. Real estate developers rely on TVM to project rental income and property appreciation. Even in personal injury lawsuits, future lost earnings are discounted back to their present value.

Key Facts

- Category

- economics

- Type

- topic